After Facebook’s most recent blowout quarter, the question is, “Where do we go from here?”

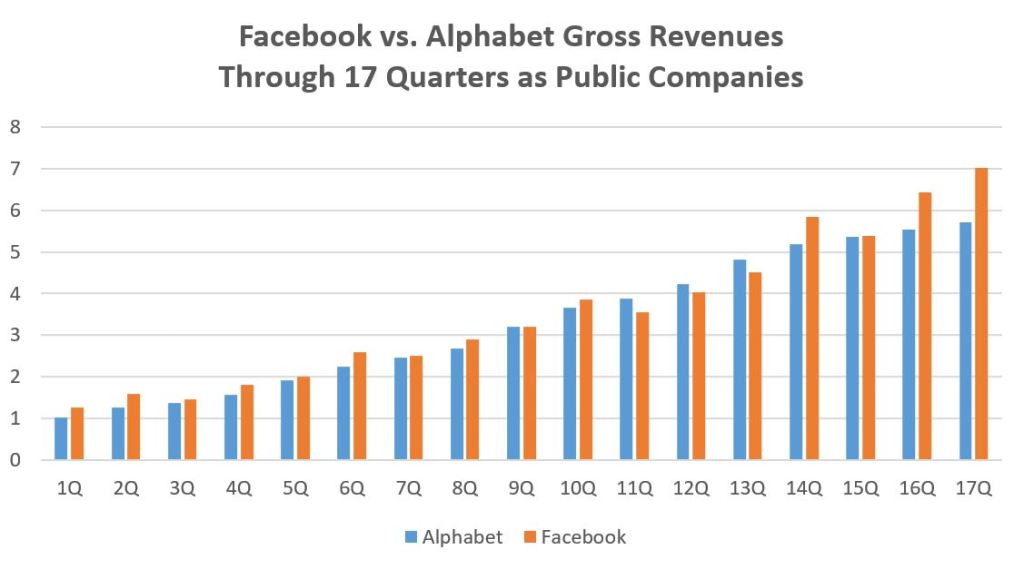

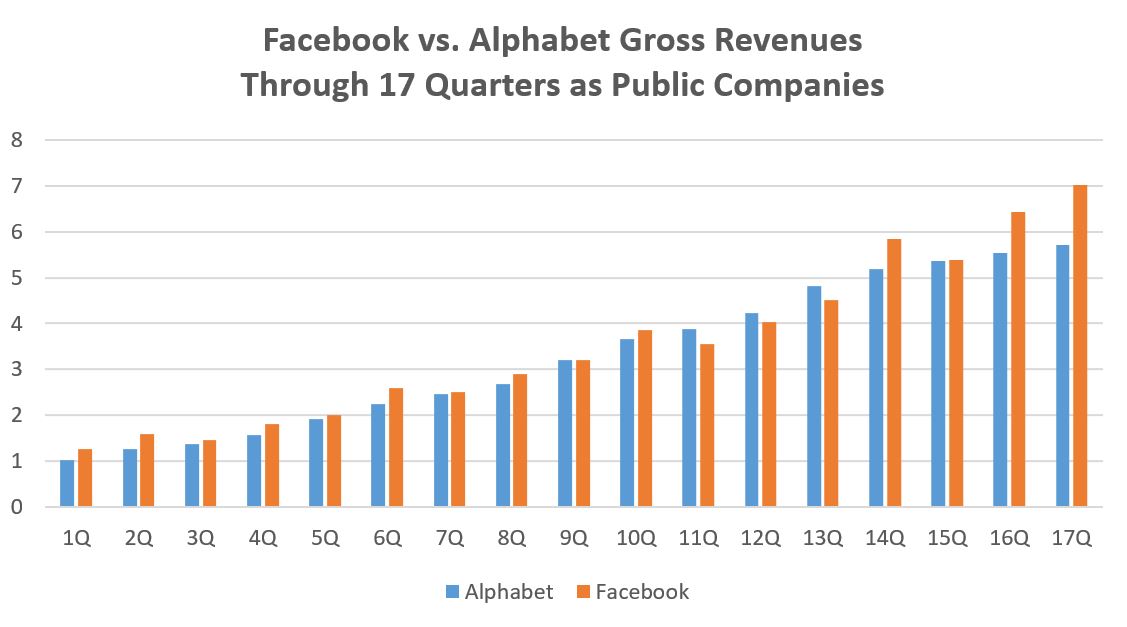

For the last several quarters, I’ve been comparing the top-line revenue for both Alphabet/Google and Facebook through their first 17 quarters as publicly traded companies. Google’s 17 quarter ended December 31, 2008, while Facebook’s ended on September 30, 2016. As the chart above shows, Google’s revenues often pace ahead of Facebook’s during holiday quarters. That was true after 13Q, for example, but not this time. Facebook has extended the lead it established in 16Q, and with 18Q marking a holiday quarter for Facebook, I expect the lead to widen even more.

I’ve used this data in the past to legitimize Facebook’s advertising platform, but that’s beyond arguing these days. Facebook and Google now consume 85 percent of all incremental dollars spent on digital advertising, and this article even speculates that the rest of the digital advertising field is shrinking. While there are pockets of growth elsewhere, these two are dominant.

How will Facebook continue to grow at such a torrid pace? After all, Facebook has three ways to increase its ad revenue. It can attract more users, those users can spend more time on the platform, and Facebook can increase ad load, or the number of ads it serves to consumers, relative to other content. Facebook announced last week that it would limit growth in ad load in 2017. With 1.7 billion monthly active users and organic growth slowing, it could acquire other audiences as it did with WhatsApp and Instagram, though there aren’t any obvious targets that would result in a big jump in unique users.

That leaves getting users to spend more time on the platform, and this is what Facebook is likely going to prioritize in the near term.

To understand how Facebook and other ecosystems grow, I highly recommend reading Dr. Richard Windsor’s blog, Radio-Free Mobile. Windsor theorizes compellingly that ecosystem revenue is correlated with share of Digital Life, which includes apps, video, search, maps, social, messaging, shopping and games – basically everything users expect to do with their phones, tablets and PCs. This framework helps explain the dominance of Facebook, Google, Amazon and Apple, as well as the struggles at Twitter.

Of all these elements of Digital Life, Facebook is arguably the weakest in shopping and games. I don’t think it’s a coincidence, therefore, that its most recent product announcements have focused on these two areas. They include:

-

Gameroom, a distribution platform for PC titles.

-

Marketplace, a competitor to Craigslist for local buyers and sellers to transact.

-

Instagram retailer tie-ins, which will enable a select group of stores to include detailed product and pricing information with its posts.

-

PayPal integration with Facebook Messenger

Leave a comment